March 30, 2009

digg_skin = 'compact'; digg_window = 'new';

Reducing emissions from deforestation and degradation (REDD) is increasingly seen as a compelling way to conserve tropical forests while simultaneously helping mitigate climate change, preserving biodiversity, and providing sustainable livelihoods for rural people.

But to become a reality REDD still faces a number of challenges, not least of which is economic competition from other forms of land use. In Indonesia and Malaysia, the biggest competitor is likely oil palm, which is presently one of the most profitable forms of land use. Oil palm is also spreading to other tropical forest areas including the Brazilian Amazon [PDF].

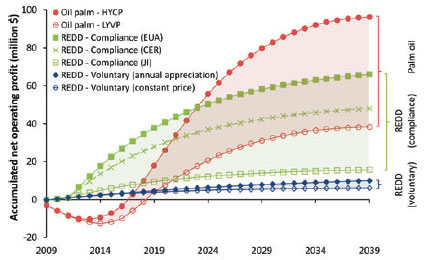

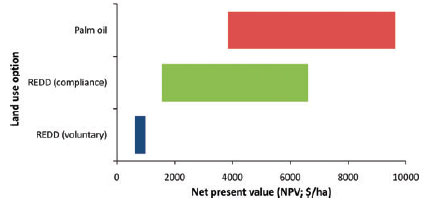

Comparing the profitability of preserving a 10,000 ha forest to reduce emissions from deforestation and forest degradation (REDD) versus converting it for palm oil production over a 30-year period. (Above) Accumulated net operating profit from 2009 to 2039. (Below) Net present values. REDD profitability is based on carbon prices of voluntary and compliance markets, including Voluntary Carbon Financial Instruments (CFI) from the Chicago Climate Futures Exchange, Joint Implementation (JI) under Article 6 of the Kyoto Protocol, Certified Emission Reductions (CER) under the Kyoto Protocol’s Clean Development Mechanism (CDM), and European Union Allowances (EUA) issued under the European Union Emission Trading System. Palm oil production profitability was modeled for the scenarios of high-yield and constant price (HYCP), and low-yield and variable price (LYVP).

To compare how REDD stacks up with oil palm, ETH Zürich ecologists Lian Pin Koh and Jaboury Ghazoul and I devised economic models to evaluate returns from each land use under different price scenarios. We found that as long as carbon credits from avoided deforestation is limited to voluntary markets where it fetches 10-20 percent of the price in compliance markets like the European Union's Emission Trading System, REDD will fail to be competitive with palm oil.

Our analysis reveals that the development of the concession for oil palm agriculture will generate a net present value ranging from $3,835 to $9,630 per hectare over a 30-year period.

Under the second scenario of REDD, we determined that voluntary markets will limit REDD operating profit to $614-$994 per hectare in NPV over the 30-year period--substantially less than profits from oil palm conversion. However, giving REDD credits price parity with carbon credits in compliance markets would boost the profitability of avoided deforestation to $1,571-$6,605 per hectare, and possibly as high as $11,784 per hectare if carbon payments are front-weighted, that is, if credits are allocated and sold during the first 8 years when deforestation actually occurs instead of distributing the credits over the full 30 years.

We believe our results are applicable for both market and non-market mechanisms for compensating tropical countries for avoiding deforestation. We of course recognize that economics isn't the sole determinant of land-use decisions, but it is nevertheless an important one. Furthermore, other ecosystem services — including biodiversity conservation and watershed protection — that may be derived from avoiding deforestation would also augment the environmental and socioeconomic benefits of REDD schemes.

We strongly believe that REDD will be more widely adopted under a climate framework that values forest carbon at levels considerably higher than present. This could happen if REDD becomes recognized by the United Nations Framework Convention on Climate Change as a legitimate emissions reduction activity during its upcoming Conference of Parties in Copenhagen in December this year.

NOTE: Our models are freely available in Excel (XLS) format.

Butler, R.A., Koh, L.P., and Ghazoul, J. 2009. REDD in the red: palm oil could undermine carbon payment schemes. Conservation Letters DOI: 10.1111/j.1755-263X.2009.00047.x

No hay comentarios.:

Publicar un comentario